Cardano Will Fall out of Top 20 in 2026, Says Nansen CEO TradingView

Source link ]]>

Nansen Founder Critiques Cardano’s (ADA) $8+ Billion Market Cap BSC NEWS

Source link ]]>

Shiba Inu was the most popular crypto in new wallets over the past week, an on-chain analytics firm recently found. Banking was a boring subject for the Baby Boomer generation, but in the Internet of programmable money, finance is fun.

If asked to guess what they thought was the most popular first coin for new crypto adopters over the past week, many people would probably guess Bitcoin. But that doesn’t seem to be the case. Neither is it the number two crypto by market cap, the peer-to-peer network computer, Ethereum (ETH).

Shiba Inu Is Currently Cryptocurrency’s Most Popular Starter Coin

On-chain data discovered by Nansen reveals the most popular non-stable coin digital asset for newly funded crypto wallets over the past seven days was Shiba Inu.

Over that period, Nansen clocked over $56 million in SHIB tokens flow into some 12,000 new wallets. The ERC-20 token was the most common crypto other than stablecoins to appear in these balances, according to Nansen.

Shiba Inu went through a slight correction, in line with the rest of the market.

The pullback coincided with stock prices edging lower after running higher in January. Analysts and commentators widely pointed to disappointed economic data and more hawkish interest rate talk from the Fed as the reason for the rout.

SHIB Token Enthusiasts Eagerly Await ‘Shibarium’

Wrapped Ether on Uniswap and ShibaSwap is the most dominant trading pair partner for SHIB by volume. But Binance holds the most Shiba Inu in SHIB balances.

There were recent misreports that Binance has delisted Shiba Ina.

The centralized crypto exchange only, however, delisted some trading pairs that included SHIB. The Dogecoin (DOGE) inspired Ethereum meme token is on Binance to stay.

The ancient Japanese dog breed, Shiba Inu, became the face of Dogecoin, the Bitcoin-forked PoW crypto that started as a joke. It went on to become one of the most highly capitalized cryptocurrencies in history and inaugurated the memecoin segment. Then DOGE even went on to inspire the Ethereum competitor.

Today SHIB enthusiasts are eagerly anticipating the recently announced Shibarium, an Ethereum layer 2 ecosystems for launching decentralized apps using SHIB as a native token

Binance Free $100 (Exclusive): Use this link to register and receive $100 free and 10% off fees on Binance Futures first month (terms).

PrimeXBT Special Offer: Use this link to register & enter POTATO50 code to receive up to $7,000 on your deposits.

The Nansen CEO was rereferring to a prediction about Cardano’s ADA token that he made back in March

Alex Svanevik, founder and CEO of blockchain analytics platform Nansen, recently took to Twitter with a pointed jab aimed at Cardano’s native cryptocurrency. He tweeted the following: “Cardano bros never thanked me for this.”

The “this” Svanevik was referring to was a prediction that he had made back in March, stating “Last chance to sell ADA above $30B market cap.”

It seems Svanevik has been proven correct, as ADA has seen an awful year price performance-wise. The cryptocurrency is down an astounding 91.67% from its all-time high. Moreover, it is down 81% on a year-to-date basis – more than even meme coin Shiba Inu (77%).

Although ADA saw an initial short-term boost in the run-up to the Vasil hard fork back in September, it has so far failed to gain any traction since then. Despite its terrible performance, ADA remains among the top 10 biggest cryptocurrencies by market cap with a valuation of roughly $9 billion.

Svanevik’s foresight might have saved some investors from massive losses this year, but there doesn’t seem to be much cause for optimism for those still holding onto their ADA coins heading into 2023. With the industry still reeling from the FTX collapse and the U.S. Federal Reserve not backing away from its hawkish monetary policy, market sentiment remains extremely bearish.

As reported by U.Today, cryptocurrency veteran Bobby Lee predicted that another crypto bull market cycle wouldn’t start until 2025.

Svanevik’s jab against ADA is not surprising since he is a supporter of Ethereum, a major Cardano competitor. The Ether cryptocurrency is down 75.14% from its all-time high.

The long-awaited Ethereum upgrade, the Merge, has been released. With the transition from PoW to PoS network, the Ethereum blockchain will become more energy efficient. Also, miners will cease to be the validators on the network. Instead, stakers will finally take over the validation and security maintenance role of the Ethereum blockchain.

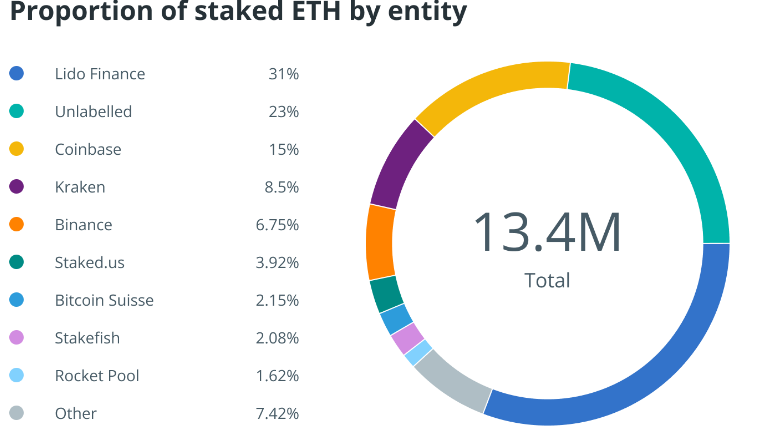

A blockchain analytics company, Nansen, gave a recent report on the distribution of staked Ether (ETH) and the significant holders. According to the report, five entities control up to 64% of staked ETH.

Lido DAO As Largest Holder Of Staked Ether

While outlining the details of its report, the firm noted that Lido DAO stands as the largest staking provider for the Merge. The DAO has about 31% share distribution of all staked Ether.

The next three more significant holders are the popular exchanges Binance, Kraken, and Coinbase, with a combined share of 30% of staked ETH. Their respective proportions of staked Ether are 6.75%, 8.5%, and 15%.

The fifth holder, tagged as ‘unlabeled,’ is a group of validators. The group controls about 23% proportions of staked ETH.

Also, the analytics firm reported on the liquidity proportions of all staked Ether. It disclosed that only 11% of the cumulative circulating Ether is staked. 65% are liquid from this staked value, while 35% are not. The report from Nansen added that the Ethereum blockchain has a total of 426 thousand validators while depositors are 80 thousand.

The development of Lido and other DeFi on-chain liquid staking platforms is for a specific agenda. First, they are to counter the risk from centralized exchanges (CEXs) as the latter amass more significant proportions of staked ETH. This is because the CEXs must operate under the regulations of their jurisdictions.

Need For Fully Decentralized Platform

Hence, DEXs such as Lido must be fully decentralized to resist censorship continuously, per Nansen’s report. However, the data from the on-chain firm showed a contrary stance for Lido.

The data indicated that the ownership of Lido’s governance token (LDO) has a tilt. Therefore, the groups with bigger token holders have more risk of censorship.

The firm cited that the top 9 addresses of the Lido DAO control 46% of the governance power. This signifies that just a small number of addresses are the dominants of proposals. So, there’s a need for sufficient decentralization for an entity such as Lido with the most considerable proportions of staked Ether.

Additionally, the analytics firm mentioned that the LIDO community is already making moves to prevent over-centralization risks. For example, it has plans involving dual governance and creating proposals for legal and physical distributed validators.

Also, Nansen highlighted the non-profitability of the majority of staked Ether. But it noted that illiquid stakers still hold 18% of staked ETH, which is in profit.

The firm mentioned that these stakers would likely engage in massive sell-offs when withdrawals become possible. However, the move will take about 6 to 12 months following the Merge.

Featured image from Pixabay, chart from TradingView.com

Blockchain analytics company Nansen linked the de-peg of Terra’s US dollar stablecoin to seven large crypto wallets, among them a wallet associated with crypto lending platform Celsius, whose massive sales of UST triggered a stampede for the exit.

UST maintained its peg to the US dollar through a complex network of arbitrageurs – traders who bought and sold the token, as well as a linked, volatile crypto called LUNA, to profit from price differences across exchanges and DeFi liquidity pools.

This all worked pretty well since UST launched in December 2020 – until the market lost confidence in the mechanism earlier this month, sending the network into a death spiral that plunged UST to $0.02 and LUNA from well over $100 to fractions of a cent.

Nansen’s report, released Friday, claims that seven arbitrageurs contributed to UST’s depegging by flooding shallow liquidity pools on Curve with huge amounts of UST.

Liquidity providers on Curve, then DeFi’s largest protocol by total value locked, are incentivized to maintain the prices of tokens in liquidity pools by balancing their supplies with other, similarly priced tokens, but huge withdrawals and inflows can temporarily throw the price of the tokens out of whack.

Using on-chain data, Nansen traced seven power users who may have triggered the depeg when they rushed to sell huge amounts of UST on Curve.

The seven wallets withdrew UST from Anchor – Terra’s lending product that offered yields of close to 20% before its collapse – sent them to Ethereum via multi-chain bridge Wormhole, then swapped them on Curve, the largest DeFi protocol, for other stablecoins.

Deluge of Sales

Right before the depeg, the seven wallets, including the one linked to Celsius, sent so much UST to Curve that the price of the stablecoin went awry.

Luna Foundation Guard – a Terra-linked organization that tried to defend UST’s peg – tried to counteract this by withdrawing about 150M UST from Curve on May 7, and adding other stablecoins back into the Curve pool.

But shortly after, five other addresses sold another deluge of UST on Curve. LFG attempted to defend the peg once again by withdrawing 189.6M UST. The war continued into the morning of May 8.

Between May 7 and May 10, Nansen reported that the top 20 addresses withdrew 2B UST from Anchor – about 11% of UST’s market cap at the time. The Block reported on May 13 that Celsius pulled out at least $500M of funds from Anchor.

But LFG’s attempts to balance the Curve pool were insufficient in the face of relentless selling. UST inflows to centralized exchanges like Binance gathered momentum on May 9. That peaked on May 10, when 165M UST was sent to centralized exchanges.

The on-chain data disputes the popular belief that a single ‘bad actor’ crashed Terra’s US dollar stablecoin earlier this month.

“While many of these wallets were likely acting independently, collectively, arbitrageurs influenced a liquidity imbalance that ultimately led to the UST/LUNA death spiral,” Nansen tweeted.

Even without Anchor, Celsius still offers interest rates of up to 9.32% on stablecoin deposits, so long as interest is paid in CEL, the platform’s utility token. The token fell sharply when UST depegged, from about $2.17 to $0.63.

Do Kwon, the founder of Terra, has since relaunched LUNA on a new blockchain, Terra 2.0. The new chain doesn’t feature an algorithmic stablecoin.